235,715

Delivered orders

Stay updated on the HECS debt timing quirk under review in Australia. Learn about the potential changes that may affect student loan repayment and plan your finances accordingly.

or a long, the Higher Education Contribution Scheme has been one of the cornerstones of how Australia finances tertiary

rogramming assignments are the tasks and projects which are assigned to the students. These assignments focus on the

F

or a long, the Higher Education

Contribution Scheme

education. It allows students to delay some of the costs of pursuing their education until they earn an adequate income.

has been one of the cornerstones of how Australia finances tertiary education. It allows students to delay some of the costs of pursuing their education until they earn an adequate income.

Recent events have, however, shown this enviable reputation, pointing to a timing anomaly in how the system works. The review will determine how that anomaly may affect graduates and what might be done to manage HECS debt.

Australian students who are qualified can defer their tuition fees using the HECS system, which means that they do not have to pay for these costs until a certain income limit is breached. Several things that make it easier for people to go to school are; repayments relative to income, CPI contingent indexation and ways of repaying voluntarily.

HECS debt refers to an amount of money owed by a student to the Australian government due to the deferral of his or her university tuition fees under a system called the Higher Education Contribution Scheme. The HECS, introduced in 1989, is a system whereby students have the option to repay fees through the taxation system once their income exceeds the minimum threshold. This loan carries no interest; however, the amount owed is indexed against inflation.

One of the conditions for HECS eligibility is that a student must be either an Australian citizen or a holder of a permanent humanitarian visa or meet specific requirements for eligibility as a New Zealand citizen. These conditions reflect the evolving admission criteria in Australia for higher education funding. By 2022, about 2.4 million Australian students were taking up HECS-HELP loans, according to government statistics. Of those young people, over 90 percent were from Australia, while about 1 percent were New Zealanders who had lived in Australia for at least ten years. This means these individuals had already qualified for this scheme during their long-term stay in the country. Additionally, students need to be enrolled in an authorized Australian higher education provider that offers Commonwealth Supported Places (CSP), which account for nearly 75 percent of all university enrollments and allow students to defer paying tuition fees. Therefore, eligibility for HECS is influenced by these factors, along with a system that delays payment until the student’s income reaches the repayment threshold.

The dynamics involved in determining the period for repaying the HECS debt are very simple: how much was lent, graduates' income, and inflation. Generally, an HECS debt would be repaid in 8-12 years by the graduates; however, for those earning less than the threshold or working on a part-time basis, it could take longer. The indexed debt rises with time, hence prolonging the payback period.

In the below section, we will be sharing some in-depth insights on Timing Quirk in HECS Debt.

What is the Timing Quirk in HECS Debt?

The Timing Quirk in HECS Debt is that the annual indexation of HECS debt occurs on June 1 each year, just before many graduates make their first annual repayment. Basically, that means that debt indexed increases in line with inflation before any repayment is taken off such that even when the graduates are about to make a considerable repayment, the amount they owe actually rises. This anomaly has been criticized for being unfair, since it could mean paying more by the graduate than would have been the case if indexation were to take place after repayment.

Implications of the Timing Quirk on Repayment

This timing quirk can have significant ramifications for graduates, particularly those close to paying off their HECS debt. For example, a graduate who was to make one large repayment in the weeks following indexation often feels penalized by such a system when the debt they are repaying has just increased. This is frustrating for those who might have carefully planned their finances and find their debt grow unexpectedly. The fact that this timing issue is under constant review hopefully is going to alleviate these concerns and make the system much fairer for all graduates.

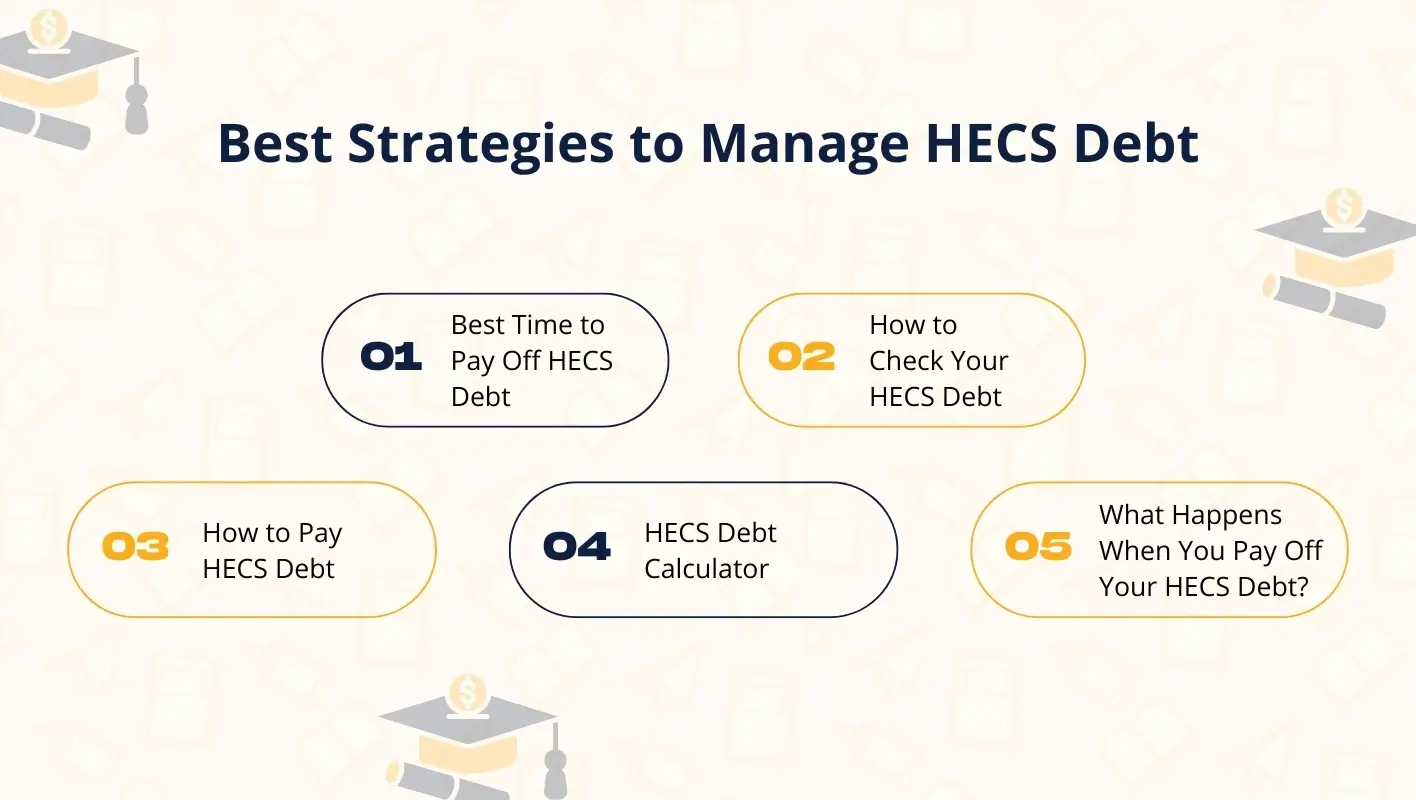

Managing HECS Debts requires some strategic planning. Some of the strategies are given below:

Best Time to Pay Off HECS Debt

Understanding the best time to pay off the HECS debt will help reduce the effect of the timing quirk. Prepaying the amount before June 1, the indexation date reduces the principal amount before it increases. This is especially effective for those who are close to paying off their debt, as it does not grow unnecessarily.

How to Check Your HECS Debt

HECS debt can be checked through the ATO website and myGov portal, where they have provided clear instructions on how to do so. You can log in to your myGov account in order to view your HECS debt balance by selecting the ATO services section. In that section, under “Tax” you will find “Loan Accounts” where you can check your current amount owed.

How to Pay HECS Debt

The HECS debt of graduates whose incomes exceed the minimum repayment threshold- increased annually- is repaid through the collection of income taxes. More specifically, repayments are calculated concerning one graduate's income: 1 percent in case one has just passed the threshold and higher in case one gets more. Moreover, at any time at their own discretion, they can make voluntary repayments through an online facility on the ATO portal or via BPAY. The repayments you make are voluntary payments that reduce the principal amount of the debt and may help manage the timing quirk.

HECS Debt Calculator

A HECS debt calculator is something that would make much sense to a graduate in order to get an idea of how long the debt will take to pay and the eventual amount paid. In fact, such calculators estimate the time of repayment by taking into consideration a person's income, threshold of repayment, indexation rates, and a number of other factors. The graduates can make better decisions on how to handle their debts using a HECS debt calculator.

What Happens When You Pay Off Your HECS Debt?

Once your HECS debt is fully repaid, you will be contacted by the ATO to confirm this. No more repayments are deducted from your income. You are thus advised to monitor your repayments closely, especially to the tail-end of your debt, so as not to overpay through the ATO. Any amounts overpaid in excess of the debt amount are refunded by them.

Given below are the impact of the review on the Future Graduates:

Potential Changes to HECS Repayment Schedules

The review of the HECS debt timing quirk may result in changes in the way and time indexation was done and in the repayments of HECS debt. One thing it could do is shift the date of indexation to after the annual tax assessment has occurred, so that repayments are applied before the debt increases. This can make the system more equitable and more transparent, and hence easier to deal with by graduates themselves.

How to Prepare for Possible Adjustments in HECS Policies

Graduates and current students should remain well updated about any of the HECS policies' changes that this review should come up with. There will be a need to clearly communicate the policy announcements and grasp what could have an effect on the repayment schedule. For example, a change in the date of indexation may affect, in turn, the timing of voluntary payments. Preparation and flexibility will, therefore, be leading principles toward readying the future adjustments.".

Assignment World offers assistance with HECS Debt. Some of the key reasons to opt for us are:

Expert Guidance on HECS Debt Management

Assignment World has a team of professionals who understand the intricacies of HECS and can assist in devising a plan that will minimize your debt by leveraging this timing quirk. We'd be happy to help you figure out when to make voluntary repayments or help you work through how indexation really works.

Personalized Support for HECSRelated Queries

We offer one-on-one consultations on all your inquiries about HECS. Whether you are currently enrolled or an alumnus, our team can answer your questions and provide personalized advice about your situation. From finding out about the eligibility criteria for HECS to obtaining information about the current status of your debt balance, we guide you through it all.

Confidentiality and Customized Solutions

At Assignment World, your privacy and confidentiality come first. The consultation and support services provided are discretion-based, which allows us to ensure that private information is protected. Furthermore, personalized solutions tailored to individual financial situations allow you to manage your HECS debt based on what's best for you.

This review of the HECS debt timing quirk is imperative to ensure that the higher education funding system in Australia is fair and equitable to all graduates. It is with a proper understanding regarding how the HECS system works, being aware of the timing quirk, and using effective strategies in managing your debt that you can keep the financial effects to a minimum and pay off your HECS debt more efficiently. As this review unfolds, being as informed as possible will help make any eventual changes that could be done more understandable and easier to cope with.